Bank of America: Dental Practice and Commercial Real Estate Financing

Refinancing from an SBA loan to a Conventional loan can potentially offer significant savings to dental practice owners for both their business and commercial real estate loans. These savings are a result of the difference between a variable high interest rate with SBA loans (usually between 7.5-9%) compared to a fixed low interest rate with Conventional loans (usually between 5-6% in today’s market).

Characteristics of an SBA Loan: For your practice or building

- Variable rates based on a Prime Plus interest rate model. Rates can spike if market conditions shift, making budgeting and managing cash flow tricky.

- Strict covenants, pre-pay penalty requirements and government oversight can impact flexibility long term.

- Personal collateral (residential real estate) is often required.

- Longer term loans can make selling a practice or building challenging, as well as minimize the profits of a sale.

Characteristics of a Conventional Loan: For your practice or building

- Fixed rates help support consistency and cash flow stability.

- Flexible structure options with lower pre-pay requirements.

- No personal collateral required.

- Multiple term options from 10-20 years to align with practice goals, as well as 100% financing scenarios.

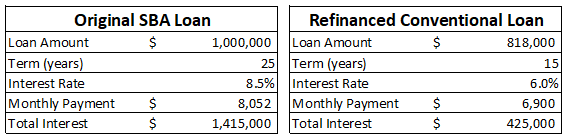

Real World Comparison

This comparison assumes the original SBA loan scenario below, as well as the borrower making equal payments for 10 years of the minimum amount. Over that time the borrow makes 120 payments totaling $966,000 which includes $784,000 of interest. The remaining loan balance is then refinanced to a Conventional loan.

*Data is for modeling purposes only.

Over the total financing life span the borrower will save more than $200,000 in total interest paid with a refinance at the 10-year mark as opposed to paying the original loan to term. They will also save almost $14,000 a year on the monthly payments which can be used re-invest in the practice to drive revenue growth.

Refinancing and consolidating existing debt for your practice and commercial real estate loans can be a powerful tool to accomplish the goals you have for your business. Not only is there potential to save significantly on total interest paid over the life of the loan, but freeing up cash flow to invest back into the business is one of the primary ways to drive increased revenue for the business. Typical benefits include:

- Investing in equipment upgrades or staff training

- Removing personal collateral that are typically associated with variable rate SBA loans.

- Improve cash flow, with lower monthly payments you can reinvest in your practice:

- Hire an associate.

- Expand services and procedures.

- Boost marketing to attract new patients.

With today's competitive lending market, you might qualify for better terms than when you first borrowed. Refinancing into a fixed-rate mortgage protects you from rising interest rates, ensuring predictable costs. It's about working smarter, not harder, to build your practice's future.

1 All programs subject to credit approval and loan amounts are subject to creditworthiness. The term, amount, interest rate, and repayment schedule for your loan, and any product features may vary depending on your creditworthiness and on the type, amount, and collateral for your loan. Bank of America may prohibit use of an account to pay off or pay down another Bank of America account. Repayment structure, prepayment options and early payoff are all subject to product availability and credit approval. Other underwriting standards and restrictions may apply. Products and restrictions are subject to change.

2 Bank of America may prohibit use of an account to pay off or pay down another Bank of America account.

3 Owner occupied commercial real estate will be determined in underwriting and requires occupancy by the borrower/guarantor. Please note SBA guidelines require at least 51% occupancy to be considered Owner Occupied.

Bank of America and the Bank of America logo are registered trademarks of Bank of America Corporation.

Bank of America Practice Solutions is a division of Bank of America, N.A. | ©2025 Bank of America Corporation | MAP7647445 | Rev. 08/26